Steen’s Chronicle: The macro narrative is changing

The new sentiment being heard from the world’s capitals is one that is familiar to investors but has long appeared alien to policymakers: doubt. Photo: iStock

- Global policymakers, central bankers starting to diverge

- Low interest rates, lowered currencies come under fire

- Political class may be nearing an existential crisis

- Banks, USDJPY, China, and oil remain the key catalysts

At the moment, it seems as if policymakers and political elites have begun to depart from the « new nothingness » consensus with the recent G20 summit in Shanghai seeing a promise not to manipulate exchange rates and the International Monetary Fund’s annual meeting in Washington even playing host to an attack on low interest rates.

What has scared such bodies away from their previous consensus?

Macro overview: the noise

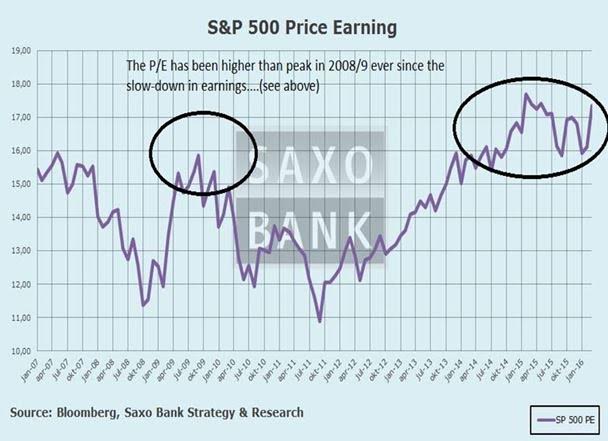

Frustration and lack of conviction are the two main themes for most investors in world markets right now, and with good reason. The S&P 500 has been trading in a broad range between 1,800 and 2,150 since 2013.

Source: Bloomberg, Saxo Bank

Of course, this is hardly surprising considering that we have no growth, no reform, no productivity, no inflation, and low-to-lower policy rates from central banks across the board.

Over the weekend I read a considerable amount of “research” and most of it concludes, as per usual, that we will continue to climb the wall of worries. This may be so, but not for the reasons most people cite: inflation returning, central bank support, higher commodity prices, and more growth on its way.

One net consequence of no top line growth and soft earnings is that we pay more for every (US) dollar’s worth of falling earnings that we see.

Reported earnings have been flat-to-negative in the S&P 500 since mid-summer… and less earnings equals higher multiples (17.35, to be precise).

This means, of course, that investors believe that « in the future » there will come better corporate results; there exists a belief that we will eventually draw away from the earnings recession we see at present.

So how about that « future »?

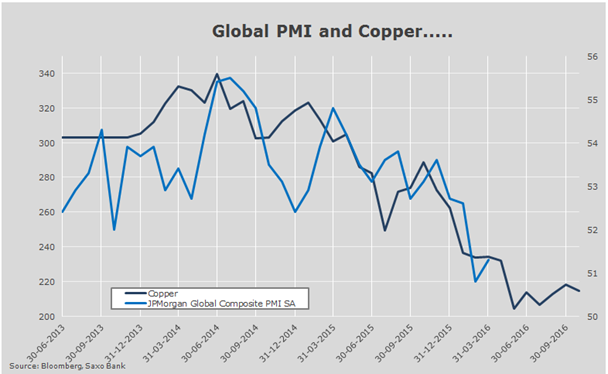

Well, a look at the JP Morgan global PMI versus copper price chart does not indicate that any such change is coming. In fact, further downside is forecasted. Here we see that copper leads the JP Morgan global PMI indicator by six months.

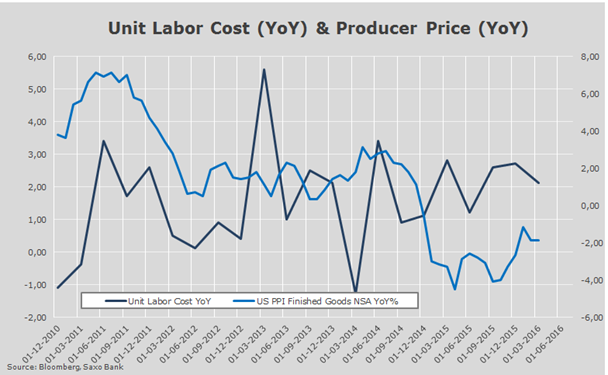

At least inflation is picking up, though – no?

Not really, as it turns out. What really matters for companies is the producer price reading.

The gap between the dark blue line (higher) and the light blue line (lower) represents a negative margin… right now, unit labour is rising higher than PPI, which is actually falling.

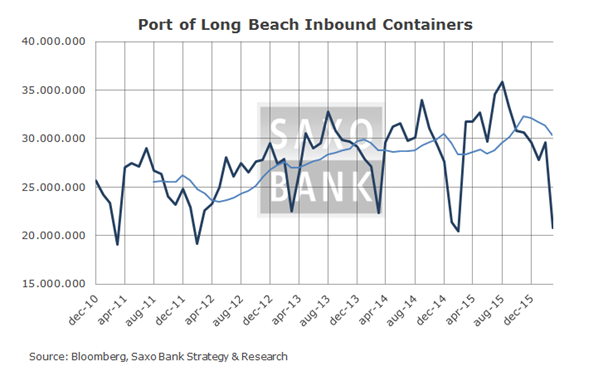

It also seems as if US industry is slowing down significantly. Here, we can see a sharp drop-off in inbound US container traffic to the port of Long Beach (the second-largest US container port, and the key gateway into the US economy from Asia).

This batch of data leaves much to interpretation; all momentum-based models are long risk here, but they remain on very thin ice. In the long term, let’s remind ourselves that S&P 500 returns simply correlate to earnings, and to increase earnings you need to increase margin.

As we can see above, of course, margin is under severe pressure as the PPI is negative and unit labour costs are slowly rising.

The most likely response from policymakers will be « more of the same », but it seems as if the political class no longer fully stands behind « manipulation ».

The new agenda: not FX, not low rates, but… what, exactly?

First we had the Shanghai G20 summit where US Treasury secretary Jack Lew delivered a promise “not to manipulate the FX rates”. Now, when we look at the IMF’s annual meeting, we have the Financial Times reporting that low interest rates themselves are coming under attack.

More interesting, perhaps, than the headline issue of low rates is the list of key topics listed by the FT further down the page:

« In a series of potential obstacles, they cited weak productivity, the lack of further firepower from monetary policy, China’s difficulties in rebalancing its economy, strains in oil exporters, disorderly capital flows, a continued impasse in talks over lending conditions to Greece and Britain’s potential exit from the EU »

This means that in the fourth month of 2016, we have very nearly come full circle. The Federal Reserve has lowered the number of slated/planned rate hikes from four to zero(?), the Bank of Japan took a (very unsuccessful) shot at a zero interest rate policy, European Central Bank president Mario Draghi whipped out his « bazooka » and implemented yet another handout to the banking sector, and now we are being told from summits in Shanghai (G20) and Washington (IMF) that none of this even works!

Has the uncertainty of the world economy finally swayed the seemingly rock-solid certainty of elite policymakers like IMF head Christine Lagarde? Photo: Wikimedia Commons

The narrative, it would appear, has changed.

The world economy, as seen from the perspective of policymakers, is on the edge of a further slowdown. Yet another crack is developing (if not being discussed) in the banking sector, but we are now being led to understand that the panacea, according to G20 leaders, is not weaker currencies or low interest rates.

So what is it?

According to the IMF, the solution is to boost employment and productivity while continuing to maintain low interest rates and draw down austerity in those countries that can afford it. Ultimately, this is the usual « half-pregnant » approach – how can one give productivity and employment a shot in the arm under such conditions?

From my perspective, we are seeing an increased awareness among world leaders that simply applying “more of the same” will take the political system down.

The « change » here is not that policymakers are acknowledging the mistakes of the past, but that they are displaying a near-desperate need to align themselves with the « broken social contract » argument, which is to stop “helping the 20% of the economy that produces 0% of the jobs and productivity” and to focus on jobs.

Whatever the “new paradigm”, it’s clear that politicians and key G20 policymakers are busy distancing themselves from their central banks (as seen, for example, in German finance minister Wolfgang Schäuble’s assertion that Mario Draghi is behind the rise of the right-wing Alternative für Deutschland party) .

This is bad news for markets. The « central banks to the rescue » model is fading – not disappearing, but fading – and if confirmed, this could the shock that wakes up the « long-only » crowd who are not only fully loaded again (the most overweight in years, actually) but who are also increasingly paying through the nose for stocks, as was demonstrated above.

Macro overview: A tactical view

I have long argued that there are three major catalysts to keep an eye on:

- Banks’ performance relative to overall indices (US, Europe and Japan).

- USDJPY as a proxy for risk-on/off and USD strength.

- China/oil as proxies for global growth itself.

The noise remains omnipresent, of course, in the form of global risks from the Syrian refugee crisis to the downfall of Dilma Rousseff’s government in Brazil; from South Africa to the Brexit; and from the « central banks to the rescue » model to less central bank leverage…

…and all of this adds up to more uncertainty, not less.

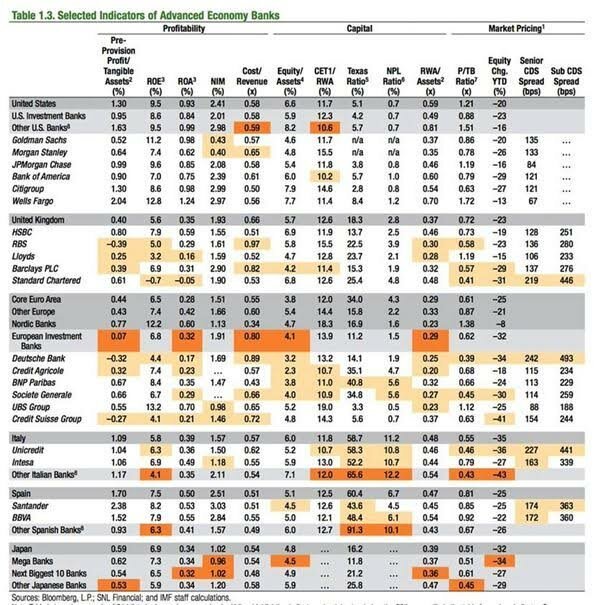

In focus: the banks

Banks are doing OK right now, but they still lag below the main indices (and for good reason given ZIRP, flat-to-inverted yield curves, and increased regulation). Ultimately, however, the cracks are widening in Italy, Greece and Portugal while US banks have finally started taking higher writeoffs on their energy investments (with more to come?).

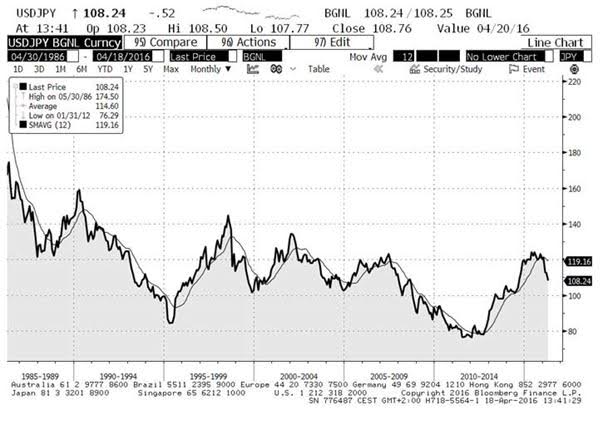

In focus: USDJPY

USDJPY remains under pressure, and one good old FX traders’ rule is to respect the 12-month moving average, which is pretty good at capturing the trend. In this pair, it’s indicating more JPY strength and not less – and don’t forget that the BoJ has a monetary policy meeting coming up on April 28.

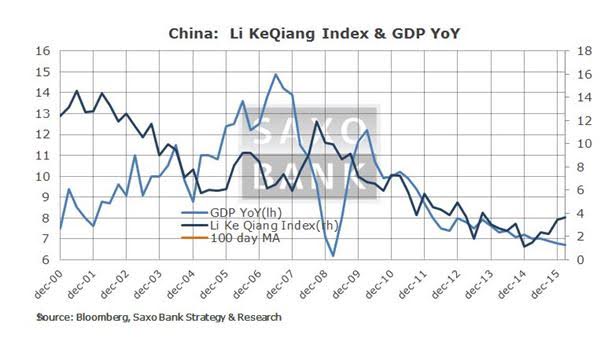

In focus: China/oil

The failure of this past weekend’s Doha summit to produce a production freeze deal was a big disappointment, whatever the market says. The inflation and oil bulls are running out of ammunition and were it not for the oil strike in Kuwait, oil markets would have seen a $3-4/barrel loss today.

China’s stimulus efforts are doing better, but once again it’s mainly credit-driven and even in China, you can only spend your money once. What this means, of course, is that more spending means less spending in the future… but the trend is clear. China is moving towards less growth in a stable manner, leaving nothing in the forecast (for now) to significantly boost global demand.

Allocation

I have moved to very defensive stance on allocation – I remain long mining and Gold, some HYG for carry, and now with 50% cash…. The price action/momentum makes market long, but for me too much doesn’t add up – the gap between perception and reality is about to be closed – hence defensive….

Short US$, long Gold, JPY and AUD – long HYG, GDX and GLD.

Safe travels,

{kind=link}

Excellent article, and very well spotted topic .

The mainstream economic narrative has indeed become much grimmer, to the extent that the anglo-saxon press now openly questions the outcome of the monetary policies endorsed by central banks.

A key fact , worth noting in support of the viewpoint expressed in this article, is the secret meeting recently held by Mrs Yellen and president Obama, organised in emergency after the GDP figure was forecast down to 0.1 percent.

http://dailyreckoning.com/fed-chairman-yellen-tell-obama/