The policy makers Comical Ali strategy

I am writing this Chronicle from South Africa which is almost as far away from Europe and the constant and never ending Brexit talk you can come. It’s hard even here to avoid the turbulence and never ending ‘need’ for investors and media to understand what comes next.

The best analogy I can use is one from my extensive travels: When you arrive at airport to check in you have to pass security control two options is at hand: The fast track or the slow version(economy class) Using the fast track gets you faster to the gate and allows you pre boarding, but what really should matter is that the actual flight time and route is the same for everyone in business and in economy. We arrive EXACTLY at the same time.

The point? What is now transpiring in an economic sense is that we have entered the fast track courtesy of Brexit, the sell of in GBP, the lowering of growth projection and in some places talk about reform and change would have happened with or without the Leave vote.

UK’s problem remains their double deficit. The chronic budget and the current account Deficits. The last time UK ran a surplus on the current account was the year Italy won the World Cup in Spain and the top scorer was Paolo Rossi, you guessed it: 1982!

Paulo Rossi, 1982

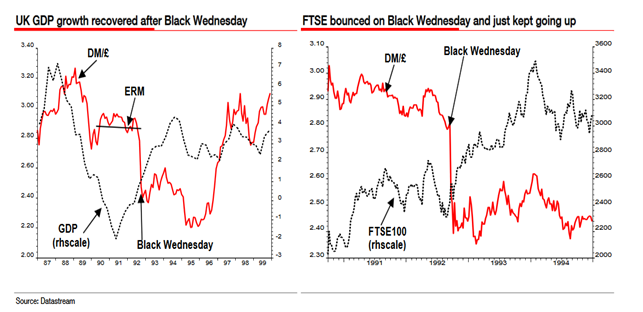

UK also have the lowest productivity of the G7 countries together with Japan. Yes, UK needs the lower GBP and desperately so and if the ERM crisis(1992) is any guideline what comes next for UK is more employment and stronger GDP as seen in this chart from the excellent research done by Societe General.

It would be naive to anticipate only positive changes from an increased political uncertainty but do realize that the slow down in not only UK but also Europe was happening pre the surprise Leave result :

The much needed change that the voters indicated is needed will come, but the macro policy makers, the politicians and central bankers, will have one more attempt at selling us an economic model of more intervention and less rigid compliance with both the EU treaty and the economic laws:

For those of you who has forgotten your economics one-on-one here is what five years in University should teach you:

The real drivers of growth is productivity, demographics, basic research and education and as little as possible red tape and intervention(no macro please)

This should be supported by a market model where capital is allocated to the highest margin return(This rule and the principle of compounding is the only thing you NEED to understand in economics)

Finally of this should be upheld by a Constitution which makes the legal system independent of government and based on respecting property right, human rights and freedom of speech.

Rather simple yet, let me ask you how many countries quality in today’s world? Few I can think off.

The macro policy makers are now the economic equivalent of Chemical Ali, the Iraq Minister of information, who claimed on live tv during the invasion of IRAW in 1993, that IRAQ and Saddam Hussein were winning the war against NATO troops while you in the background saw the American forces moving forward inside the lense of the camera!

Comical Ali, 2003

The early response from EU and its leader has been one of ‘sadness’ and a rhetoric line which followed the totally inept scare mongering which preceded the vote.

Trust me come end of next week everyone and their dogs will be looking for more soft and open arms policies in the discussions with the UK. I noticed that the Father of the EU former Chancellor Helmuth Kohl was out in German media this morning calling for exactly that: Kohl fordert ‘Atempause’ fur Europe (http://mobil.n-tv.de/politik/

UK will be the largest country in population by 2030 in Europe, it’s has the biggest military might and the single largest concentration of capital markets and talent outside the US – furthermore the UK runs a massive deficit with Europe, so if the European leaders wants a future Europe/NATO/EA without active participation by the UK military, capital markets, consumer demand, and deficit then please carry on acting like a bunch of cry babies.

The next macro response will have three tracks.

A revisit to 2009 macro policies

EU will try to sell a message of moving forward, but the deep rooted difference between Germany and France on the future of EU will make for an impossible act.

Germany wants reforms of Europe to make the way for more consolidation, while the French wants to skip all the reforms and reach a European Super State and then work back from there.

Major difference…this leaves open a patchwork of deals and bartering where Italy’s Renzi probably will be allowed to do state support for the banks (because if not Europe will be under attack), Greece will get another free pas and France plus Club Med can again expand deficits not only in excess of 3% deficit but almost infinitely. Yes, this a going to be total remake of the action taken post the fall out in March 2009.

The problem.. We are saturated with low interest rates and QE, 75% of all QE goes to keep existing debt in place and with that being the number one priority there is little scope or chances for CAPEX and growth to come back. We have simply crowded out investment and productivity by trying to buy more time.

Dogmatic Fed and other major central banks will move deeper into negative yields

Fed started the year promising us, no guaranteeing us that they would hikes rate 3-5 times in 2016, now the market believes there is more chance of a cut than a hike next time Fed moves. In the process Fed has become predictable (never listen to what they do, but act on what they do do – which most of time is nothing) and lost what little credibility they had left in the process.

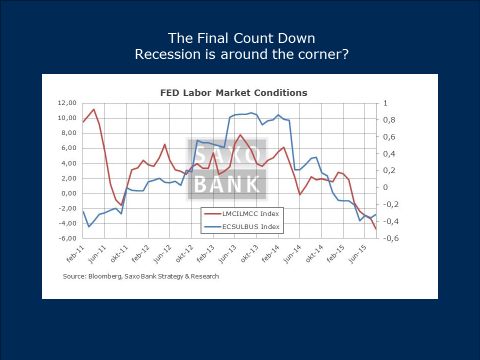

Fed will not hike in 2016 and recession is now more than 60% likely as Feds own Labor Market Indicator continues to make new lows and Conference Boards Leading Indicator goes down in sympathy.

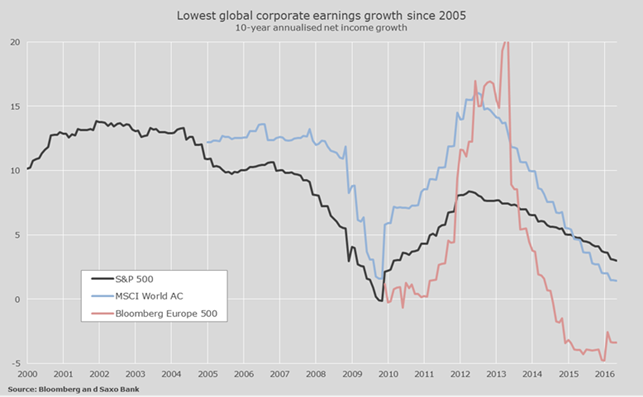

US corporation earnings is lowest since 2005 as my colleague Peter Garnry pointed out this week. In other words US will be lucky to get 1.5% growth this year and we remain more likely to see more downside if the above macro push fails either fails to materialize or get delayed or diluted by the usual compromises.

Bank of Japan will move after the July Diet election in Japan. There is now talks that Prime Minister Abe is ready with a fiscal plan to the tune of 2% of GDP, but really… We all have that t-shirt, we have been there before. It will give a short term bump to growth but increase debt and hence leaves them worse off. Reforms creates growths. Not more debt.

It’s about the Social Contract being broken stupid!

Finally, the social contract will remain broken. The US election is up next as focal point and with a Trump vs. Clinton race we are guaranteed a lot of entertainment but also two people who is the White House will upset the normal routine. Ms. Clinton has been forced to the far left by Bernie Sanders, who is likely to be the King Maker in the Democratic Convention, while Trump…well he is Trump.

Source: Zapiro – South Africa

(I guess everything is relative Trump seen from South Africa who has enough trouble of their own)

Ms. Clinton is running on a anti business ticket and Mr. Trump is running on anti establishment ticket. None of these two tickets is good for Wall Street, Pharma or stock markets. I predict Trump will do significant better come November than the present ten point spread. (Just rerun the Brexit vote…) – I have gut feeling, like I did with Brexit that Trump carries the White House by January, but I think personally both of the candidates stands out as being the worst choice given ever to the US voter.

Trump will be bad for the US Dollar of that I have no doubt. His so called foreign policy is not only backwards but will have companies flee America.

Clinton will be bad for banks, and other ‘capitalists ». She did try to do this job, undermining corporate US when she was wife of President of Bill Clinton, but somehow a deal with some cigars got in the way……

Anyone who is anti establishment is electable in any referendum globally. It’s not about the political programs or their visions is about unseating the status quo …sad but we are witnessing a true low in politics right which is think will coincide with a new low in economic activity, inflation and growth over next three month. Markets will trail this timeline by three to six month, which to me means low is in by summer 2017.

Conclusion

The Brexit will be a catalyst for change. I will ultimately stop the pretend-and-extend because new deals is needed. The biggest fall out will be political. A whole generation of politicians is lost. Their project of buying time, being unaccountable and constantly applying more debt to any issue has been sutured and is crowding out changes.

Come summer 2017 we will see a much weaker US dollar (1.35 EURUSD), higher Gold, a stock market which has been down 20-25% before recovering and new lows in government debt yield in G7.

A classic Permanent portfolio will be my approach personally, making sure I am reweighted into more risk when market is down and taking off profit when it’s up.

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!