Global deflation it ebbing out – Is inflation coming back?

Answer: Yes, it is!

The main impact though will be less consumer spending as China’s low export prices has kept the US consumers in play through ever lower prices – this is now reverting – it also means weaker CNY, and higher inflation expectations from here (globally) which of course is classic end of cycle reactions, which confirms my main macro thesis:

We stand in front of massive macro paradigm shift away from “easy money” through recession to “helicopter” money.

Source : Bloomberg – China PPI YoY & OECD CPI

This is China PPI YoY (now positive) and correlated to OECD CPI inflation – clearly China has played a central role in the disinflation (or deflation)….and it’s why inflation despite massive QE has been subdued.

Furthermore it’s important to understand that the falling Chinese prices have kept pretend-and-extend alive longer, as import prices in net deficit countries like US, UK, South Africa et al has been collapsing making room for stabilising or even improving purchasing power in an environment with less growth and earnings.

This trend if confirmed next few month could be major harbinger for inflation concerns coming back into focus. To me this is another sign of an end of cycle – as Albert Edwards and others have pointed out it’s pretty classic that inflation rises into….an recession – late in a cycle pricing is peaking before meeting no new demand.

Source : Bloomberg – 5Y5Y US Inflation swap

Our overall macro outlook:

Q4 and into Q1 will see tighter money market conditions combined with Fed raising rates in December – that will be the peak of the US Dollar strength and the meeker growth improvement which is coming through in Q4

(Be long US Dollar vs basket of deficit currencies: ZAR; TRY, AUD and CAD – UW: Equity & Fixed Income and OW: Cash – buy optionality on downside SPX,DAX and upside on GBP(1Y call) & CHF

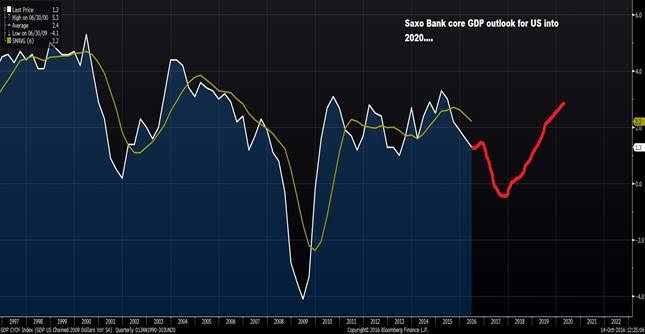

In 2017/Q2-Q3 we will move towards recession in the US – this of course coincides with an election cycle which will see voters going to the polls in: the US, Italy, Netherlands, France and Germany – (i.e: little room for fiscal support during this period..) making uncertainty the name of game.

Very few people in the market is willing to accept that Bank of Japan a couple of weeks ago changed the “lower for longer game” to one of “preparing for helicopter money” – this may be the single most important policy change in since the great financial crisis started.The new announced target rate of 0% in 10Y JGB (from negative..) is a back door opening for the government in Japan to create more fiscal deficits and through this a full helicopter money approach.

By having a zero percent targeted yield in JGB’s this is no longer any hindrance for Prime Minister Abe to go full in on further deficit creation.

Japan remains the leader of experimental economic- and monetary policy, observe how FED, BOE and ECB is trailing behind with years delay.

This new direction (target rates for government yield) will ultimately be the policy response from Europe and the US when we in 2017 runs into the next banking and economic crisis as their traditional monetary response since Greenspan, cutting steering rates, is out of order.

Conclusion

A Chinese Producer Price Index may seem a relative trivial economic indicator, but through export prices it feeds into the global inflation and China has been a powerful supporter of consumers globally through lowering the price of imports.

Now this trend is reversing to higher inflation creating a need for CNY for devalue further and reigniting inflation expectations while central banks are about to reduce their endless QE support.

This means higher prices, lower growth and stronger US Dollar which is as close as you get to a perfect mixture for a recession.

Recessions is the economic equivalent of “a clearing of excess” – I will argue what the world needs is some adjustment to reality and a recession will do that, but it will come with massive political movements, further social contract issues and increase volatility.

I will let Lao Tzu have the final words: “Life is a series of natural and spontaneous changes. Don’t resist them – that only creates sorrow. Let reality be reality. Let things flow naturally forward in whatever way they like”

Safe travels,

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!