Steen’s Chronicle : Long gold, short $ and long fixed income …

We have again and again argued that the ”forces” of the market leads one way only:

– Weaker US dollar as world would collapse with the opposite(strong dollar) under the burden of $ denominated debt

– Higher gold – as only true independent asset in world of artificial overload (plus falling US rates)

– Long fixed income – Free option (put) on equity market + coupon + recession risk (>60%)

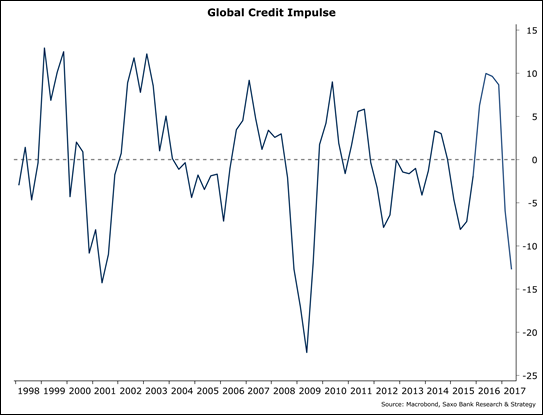

This is driven a credit impulse which in Q4 will surprise market negatively as PBOC & Fed continues to lower the velocity of credit facilitation and a strong deflation trend ignored by central bank and market in general.

We like, Albert Edwards @ SocGen, this week believe deflation is bigger risk … that 1% CPI is more likely than 2% ……in the US

Furthermore this late pm – Christopher Dembik, my colleague and head of macro, updated the Saxo version of the CREDIT IMPULSE:

This is not good news, but…. The real low (in economic activity)… will be 6-9 month from now… and in September / October we expect GLOBAL DATA, led by China and Europe to come off ….

Having said that……..and long-term staying with the themes mentioned, I now find market extended in gold, dollar and rates…which have led to me to go neutral on all three, which is 75% of my overall risk. Left in place is long gold miners…….and downside puts in NASQ and EURUSD….

The catalyst for increased dollar demand (Tvm Nedbank- South Africa – Neels and Mehul) could /will be when the debt ceiling is lifted (This will stop the US government from drawing down on reserves in the major banks (and hence increasing liquidity in the banking system…)

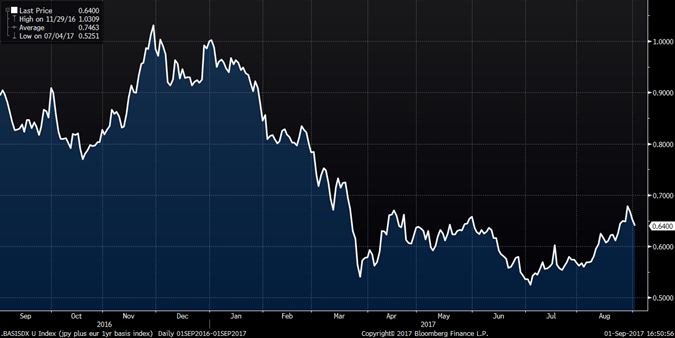

Observe the basis spreads for EURO and JPY – this chart is an INDEX where January 1 is 100… hence we have seen some “normalization” from extremely rich “funding dollars” to less so.. but still rich – We believe this is one of the main drivers of the Q1+Q2 risk on …

I will write extensive piece over weekend – Monday on this September / October likely cycle of strong US dollar through lack of funding dollar plus “true” political risk..

Nice weekend,

Steen

On attend la suite avec impatience parce que jusque là même avec un bon décodeur, … c’est pentu comme raisonnement !