FOMC – didn’t buy the deflation…..yet….

FOMC delivered as we expected but more hawkish than consensus: Saxo preview of Fed – May 1st 2019

We remain with key elements of yesterday’s view:

- If Saxo is right: small risk off – a correction inside the present bull market as technical and valuations are extremely stretched, particularly relative to economic data and earnings.

- We continue to think the market is in a sideways formation after the strong run-up in Q1. We see the next risk infliction point coming in July/August where enough time will have passed for the market to realise that improvement in economic activity is not forthcoming, particularly not from a policy response of lower funding costs. That timeline also, and notably, moves us past the conclusion of the China-US trade deal.Our risk outlook is neutral with a small overweight in long-term US fixed income relative to cash.

Action:

- The FOMC meeting – being more hawkish than expected – confirms Peter Garnry’s overall equity view of take profit / reduce magnitude of riskas market is too short volatility, too long economic growth and overall our scenario remain based inside the False Stabilisation

- US Dollar long mainly through short XAU and GBP should be preferred trades

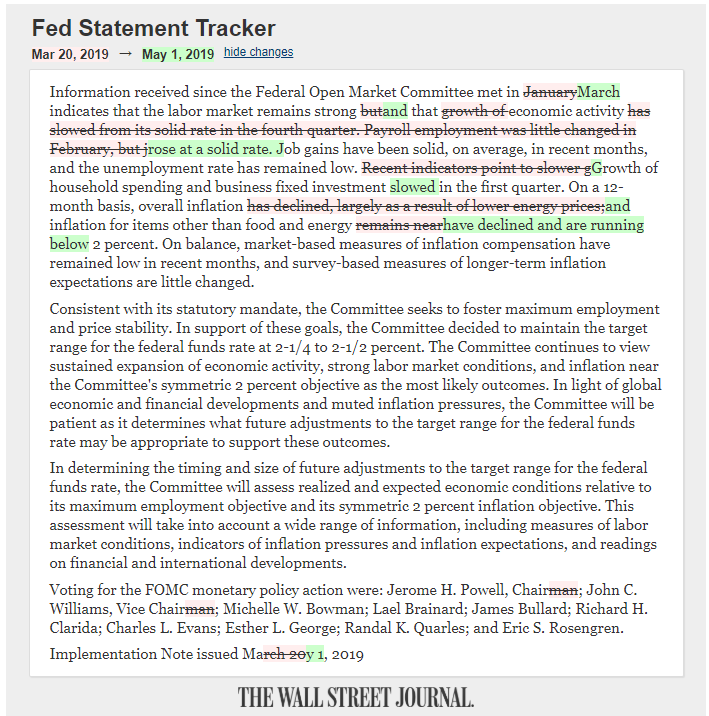

Copy-pasting from WSJ.com…plus link from me…

- Fed officials said their 2% inflation target is symmetric, meaning they expect inflation will drift mildly above and below it at different times. They seek to keep inflation at that level because they see it as consistent with a healthy economy.

- “There’s reason to think that these will be transient,” Mr. Powell said. “We of course will be watching very carefully to see that that is the case.”

- In an interview last month, Chicago Fed President Charles Evans said that if an inflation shortfall was persistent, he would support cutting rates to take out insurance against the risk of economic softness. Comment: The consensus Wall Street analysis took this statement for an imminent “insurance as in 1995 and 1998. It was delayed by FOMC yday… https://www.ft.com/content/c5d71304-5f7e-11e9-b285-3acd5d43599e

- Separately, Fed governors voted unanimously to reduce a different interest rate paid on bank deposits, known as reserves, maintained at the Fed. They lowered this rate of interest on excess reserves to 2.35% from 2.4%. Comment: Again market was seeing this correction in OIER but 5 bps was cut

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!