Macro Digest: The Italian « non-event » could be a EURCHF event

Idea: Sell EURCHF @ 1.1815 w. s/l 1.2010

Why?

- Uncertainty of new Italian government commitment to Europe and EUR

- The fiscal expansion risk down-grade, higher spreads, and more uncertainty.

- EURCHF correlates well with risk premium on Italian debt in 10y (10Y Italy government yield minus 10 Y German yield)

- EURCHF broken down on our long-term monthly model – which uses 12 SMA a long or short

The Italian situation remains uncertain – the latest news indicates that Luigi Di Maio, 5 Star, and Matteo Salvini, League will meet today to finalize program before presenting it to President Sergio Mattarella before or on Monday. There is some “event risk” over week-end.

It seems unlike that either Maio or Salvini will be Prime Minister(although 5 Star still put Di Maio forward), the leading candidates according to Politico is:

Politico – Italy what happens next?

Mr. Wolf: Alfonso Bonafede is a 5Star parliamentarian whose name has been floated in Italian media for two days as a potential prime minister. A close ally of the movement’s leader Di Maio, the 42-year-old native from Sicily is a lawyer by training and has built a reputation for being a problem solver, hence the nickname “Mr. Wolf,” a reference to the fixer in Quentin Tarantino’s “Pulp Fiction.”

https://it.wikipedia.org/wiki/Alfonso_Bonafede

The shadow man: Vincenzo Spadafora is described by Italian media as the éminence grise of the movement, the kingmaker quietly working behind the scenes. The 44-year-old Napoli native began his political career in 1998 serving in several left and center-left administrations. He already has an autobiography called “The third Italy, a manifesto of a country that does not hold back.”

https://it.wikipedia.org/wiki/Vincenzo_Spadafora

Quick summary of The Five Star Movement and Lega published program: (Main source: Goldman Sachs, European Views: An Italian fiscal expansion)

- Universal minimum guaranteed income to all citizens (Cost: 15-30 bln EUR or 1-2% of GDP)

- Reform of tax system (Cost: 64 bln EUR or 3.7% of GDP)

- Reform of pension system (Cost: 15-20 bln (1-1.5% of GDP)

- Cancelling of VAT hikes in 2019,21,22 (Cost: 12.5-19 bln. (0.7%-1.1% GDP)

This fiscal expansion will be off-setting long term commitment to debt reduction, most likely put Italy in opposition to EU and ECB, and risk a downgrade on the debt. Even a watered down version of the program will be unsettling. The market is slowly repricing risk but we estimate too slowly.

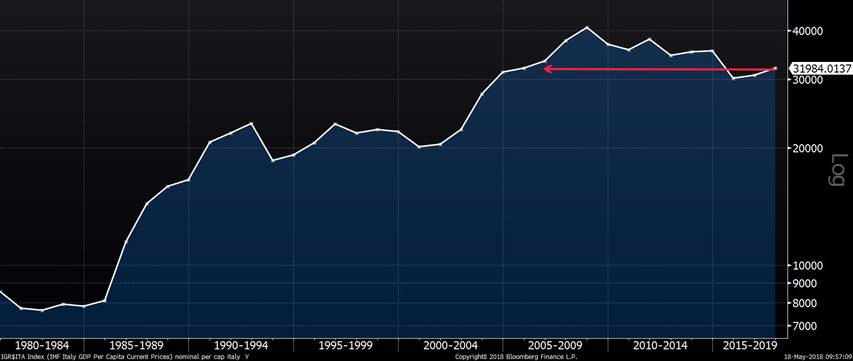

The macro situation is poor in Italy one a few countries in the world not yet back at pre-crisis GDP!

GDP per capita Italy.

EURCHF spot vs. 12 month SMA – now negative the cross

10 Y risk premium on Italian debt vs. German debt plus EURCHF spot – it would indicate “fair-value” of 1.1500

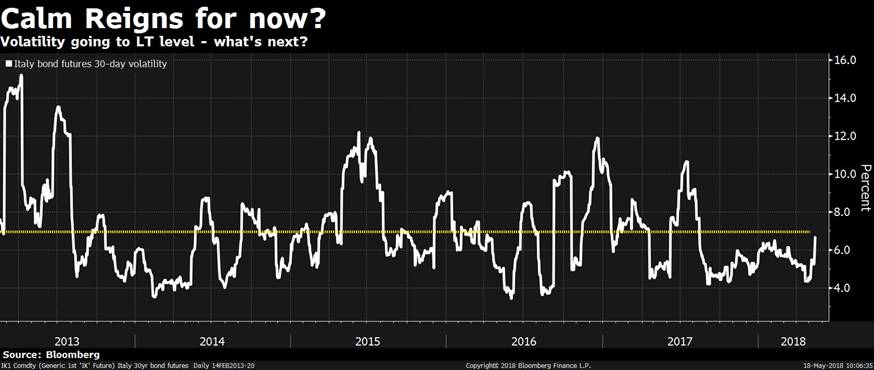

Bond market key indicator for risk on / risk off in Italy – here is Italian bond futures 30-day volatility – now back to long term levels….

Spread Italy over Germany in 10Y… recent trend

—

Ce document ne constitue ni une recommandation d’achat ou de vente, ni une incitation à l’investissement.

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!