Steen’s Chronicle: All great things are simple… except right now

While our hopes may be simple, our circumstances are regrettably complex. With geopolitical risks on the rise, the global credit impulse having peaked, and central banks relying on outdated models, Saxo Bank chief economist Steen Jakobsen says that the key concept to keep front-of-mind is mean-reversion.

- Credit impulse continues to point to imminent slowdown

- Energy prices to fall as China leads drive for electric cars

- Central banks to move away from outdated Philips curve model

- Trump, US tech sector has it all wrong on China and Asia

- Fed balance sheet no longer lending support to the market

« All the great things are simple, and many can be expressed in a single word: freedom, justice, honour, duty, mercy, hope » — Winston Churchill

Let’s start with what is currently simple, and what has been simple all year.

- The US dollar has peaked and started a multi-year cycle lower as both US and world growth can’t work without a weaker dollar (a stronger dollar kills growth through debt service, emerging markets, and commodities).

- Everything is deflationary: demographics, technology, energy, and the debt mountain.

- The credit impulse peaked in late 2016/early 2017 leaving global growth vulnerable in the fourth quarter of 2016 and into Q1’17.

- US interest rates are headed to 0% in 10-year government yields by the end of 2018, early 2019.

I am enclosing the word « simple » between a generously-sized pair of quotation marks because nothing is truly simple. But the themes outlined above have served us well throughout 2017 with the market having now given up on the Federal Reserve hiking rates beyond December. This is because inflation in the US (and Europe) is more likely to hit 1% than 2%, and because growth –despite certain green shoots – remains considerably below historically normal recovery levels.

Meanwhile, most central banks – most prominently the Fed – continue to believe in the old-school Phillips curve model, and through this mistake they misguide markets on both inflation and growth – a classically dogmatic, bureaucratic way of thinking whose limits in a world of ever-changing technology are obvious.

- New call: energy prices to fall by 50% over the next 10 years.

For the balance of 2017 and into 2018, we will add that investors should expect considerably lower energy price levels to prevail as the electrification of cars goes mainstream. This will be led by China as electric cars represent a solution to the country’s pollution problems (viewed as « social priority number one » by authorities in Beijing).

Petrol and diesel consumption by cars represents 55% of all oil consumption in the world and we deem the recent announcement by Volvo – now owned by China’s Geely (disclaimer: Geely also holds a 30% share in Saxo Bank) to be an indication of new industry standards.

These being our main long-term macro themes, let’s look at the far more confusing short- and medium-term picture…

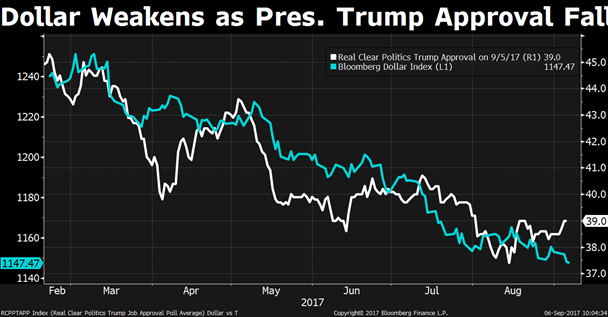

USD, Trump disapproval correlated 1:1:

Source: Bloomberg

Source: BloombergThis probably comes as no great surprise but the correlation nevertheless confirms that even if Trump were successful in his policies, it would accelerate rather than slow the weakness of the dollar.

The US runs an expanding current account deficit. It spends more money than it makes, and Trump says that this needs to be reduced. Fine… let’s do that, but let’s also realise that this would mean US living standards would fall as the current account deficit corrects.

More precisely, the ability to spend money will fall as running a deficit is like living beyond your means; a surplus is the opposite.

Sometimes facts and understanding can get in the way of politics. I know it’s sad, but a current account is one of the few things that can’t be manipulated as there is an offset with another country at the other end!

Trump’s « America First » ethos is also anti-productivity as creating jobs for the mere sake of doing so is not the same as, and cannot compete with, creating productive jobs – and I apologise for stating the obvious!

It’s clear that one of the few sectors in which the US remains competitive is technology, but the problem here also partly comes down to Trump. One of his key policies and longest-held views, after all, is that China is the « bad guy ». The US president seems committed to launching a trade war with China that, together with the US technology sector’s lack of a Chinese footprint, will give investors a wake-up call sooner rather than later.

Right now, there are four billion people living in Asia (and the Indian subcontinent). By 2050, that number will have swelled to five billion – a five billion-strong market in which the US monopolies (Facebook, Google, and Amazon) have little or no market share.

Good luck paying for 30 years of profit in a single share of Amazon given these conditions…

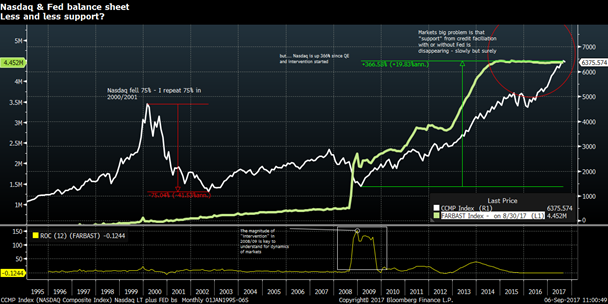

Speaking of Amazon, I have to include this next chart… when listening to the younger traders on Saxo’s trading floor, it can seem like they forget that selloffs of 30-50% are the norm, not the exception, when looked at over a generation.

This is my Nasdaq long-term chart combined with the crazy explosion of the Fed’s balance sheet…

Nasdaq and the Fed:

Source: Bloomberg, Saxo bank

To understand the magnitude of the intervention made in 2008/09, look at the rate-of-change[Steen Jakobsen] (ROC). Also, note how the Fed’s balance sheet no longer lends support to the market, but of course, negative convexity and reaching for yield carries the market forward by expanding P/Es into bubble territory… for now.

BoC leads on bubbles, Phillips curve declared dead (by me!)

The most interesting new development in central banking, however, is how some central banks are going it alone. Case in point? The Bank of Canada, which has now made two rate hikes independent of the Fed to deal with the country’s housing bubble.

House prices in Canada are up 13% year-to-date and 200% since 2000; most of this is financed by 25-year amortization on five-year terms (i.e., rates are reset at five-year intervals).

Two-year Canadian rates are now higher than their US equivalents for the first time ever, and the market is pricing in a 65% chance of another hike in December (and 40% in October).

The point? Canada’s central bankers are clearly acting on bubbles and excess while the Fed and the European Central Bank continue to monitor the non-existent link between tight labour markets and inflation.

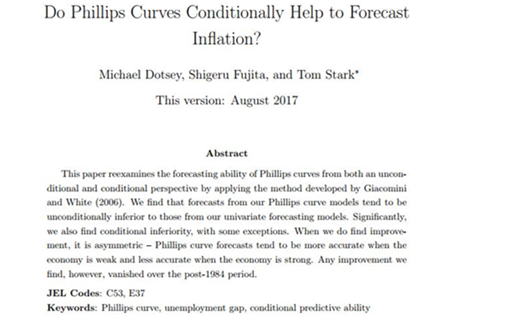

This recent working paper from the Philadelphia Fed is interesting in terms of its relation to central bank policy and show even Fed’s own staff does not find support for the link between employment and inflation:

Source: Federal Reserve Bank of Philadelphia

Why is this relevant? Because central banks’ modus operandi is to peg policy to academic papers. Remember how I alerted you to pivot on the change in central banks’ quantitative easing consensus based on new evidence which found that QE without fiscal stimulus was inefficient?

Well, I expect this paper to dictate a similar sea change away from reliance on Phillips curves and towards and increased focus on the deflationary effects of technology, demographics, and the debt burden.

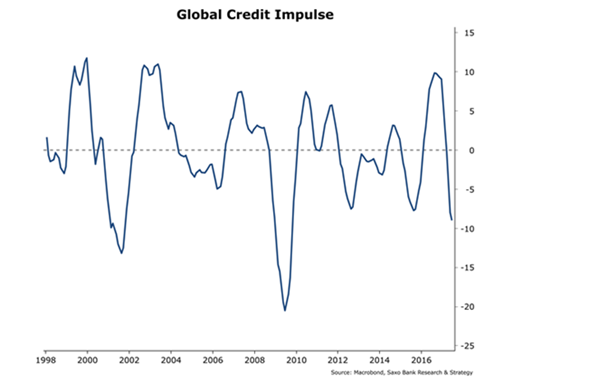

Don’t believe your eyes; the global economy is cooling

This is Saxo Bank’s global credit impulse monitor (the credit impulse is the « rate of change of change » of credit in the market = velocity of credit).

Create your own charts with SaxoTraderGO click here to learn more

Source: Saxo Bank

This indicator leads markets by nine to twelve months and the magnitude of the current slowdown almost mirrors the equivalent slowdown in 2008/2009.

I can already hear you protesting… « but the PMIs, the surveys, the data are improving! ».

Sure, but these are all lagging indicators despite their fancy names and survey-based questions.

Think of all economic and price data as having its own collective sine wave:

These sine curves (data points) move forward and will have different peaks and troughs, but what’s interesting is when they all peak or bottom. What our credit impulse model says is that from the peak in Q4’16 there is a high probability of a big slowdown in the global economy 9-12 months later – so from October 2017 to March 2018.

As I like to say, today’s economic data were created nine months ago by the amount of credit, the price of credit, and the energy prices seen following Donald Trump’s electoral win. The peak in activity seen in Q4’16/Q1’17, again, was created by massive credit creation post- the worst Q1 start in recent history (and one which drove the ECB and China to go full throttle on credit creation).

This call for a significant slowdown coincides with several facts: the ECB’s QE programme will conclude by end-2017 and will at best be scaled down by €10 billion per ECB meeting in 2018.

The Fed, for its part, will engage in quantitative tightening with its announced balance sheet runoff. All in all, the market already predicts significant tightening by mid-2018.

We argue that the market is always late to the facts, hence the slowdown is now and is manifesting into a political situation where geopolitical risk continues to rise, where Trump is a lame-duck president, and where the debt mountain continues to grow while the repayment burden increases via “too low” inflation.

This is a dangerous cocktail, particularly considering the high level of convexity and the low-volatility environment we are in.

Asset allocation

We have had the same positioning since Q1’17 (we use a Permanent Portfolio approach):

Equities: 25% (respecting the momentum)

Fixed income: 50% (see attached memo)

Commodities: 25% (overweight gold and silver)

Cash: zero

We have recently reduced some of the risk as we are now:

Equities: 10% (mainly gold mining stocks)

Fixed Income: 25% (neutral weight)

Commodities: 25% (neutral weight)

Cash: 40% (overweight)

The cash weighting, of course, is “too high” but we want to wait out September and Q4 to see how the credit impulse plays out. It’s been a good investor year and as J.P Morgan once said when asked how he became rich, “I took my profit too early”

Overall, we at Saxo Bank run several competing asset allocation models, which we are happy to share:

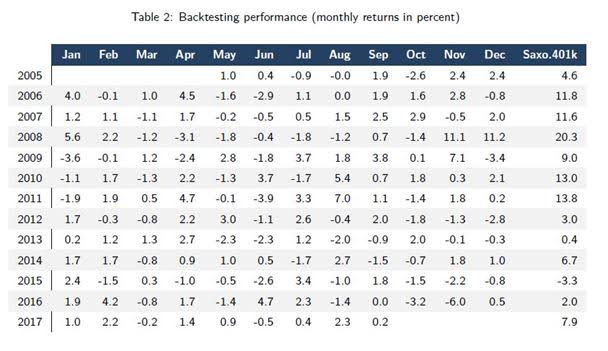

401K (geared to long-term pension):

Source: Saxo Bank

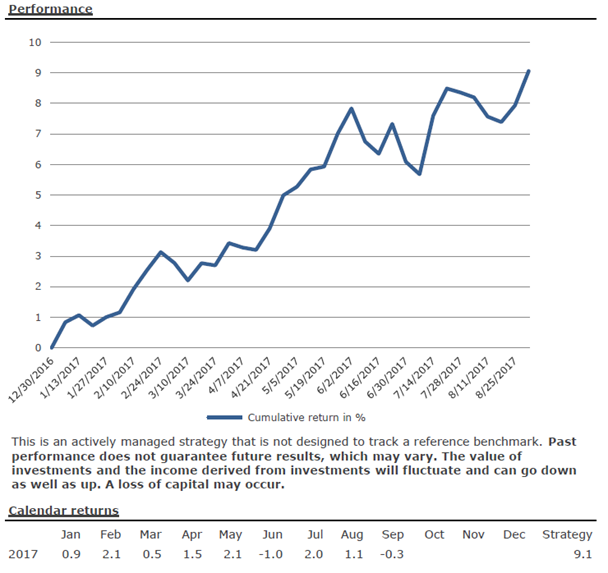

Stronghold (an asset management product tailored to reduce tail-risk (accepting a maximum 1% or 2% drawdown and with machine learning qualification of signal weights):

Source: Saxo Bank

(This defensive model has recently reduced Nasdaq exposure and rebalanced into biotech and US fixed income.)

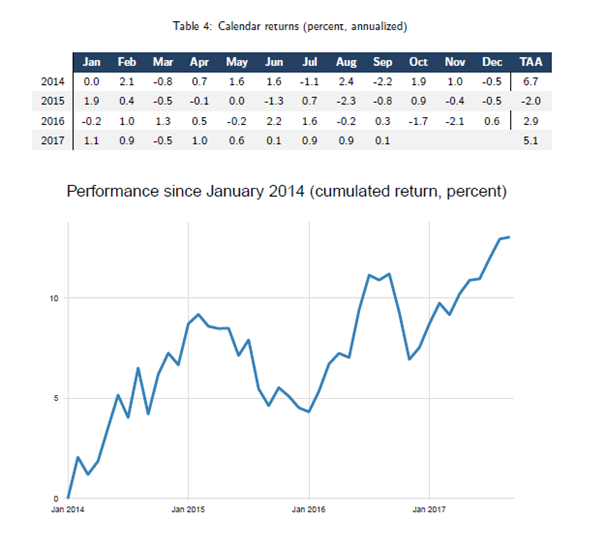

Tactical Asset Allocation (an optimised model for price distribution by assets, including short positions):

This just to illustrate that we maintain a sharp focus on asset allocation as 90% of your returns are driven by asset allocation rather than by single stocks or asset contribution.

Conclusion

I have purposely avoided discussing North Korea (where I think military escalation is inevitable); ECB tapering (which will be slow if at all); the Fed noise on Gary Cohn, Stanley Fischer and the lack of board members; the German election (major non-event); and Trump (lame-duck from here) to focus on what in my opinion truly drives the market:

- The price of credit: Rising due to policy mistakes (read: Phillips curves)

- The amount of credit: Dropping hard – contracting indicating slow-down from Q4-2017 into Q2-2018

- Energy: The trend is clearly down and year-over-year changes dictate inflation inputs and direction

So brace yourself and your portfolio for still-lower government yields, the flattening of yield curves (financial sector underperformance), and expected returns for stocks that on a good day with tailwinds will do 2-3% per annum versus 9-10% historically.

When asked for the biggest lesson learned over more than 60 years in business, Vanguard founder John Bogle answered as follows: « reversion to the mean ». What’s hot today isn’t likely to be hot tomorrow, and the stock market reverts to fundamental returns over the long run.

Is it simple? Hardly. If anything, we are moving further away the simplicity embodied by five of Churchill’s six famous words.

We are moving away from freedom in terms of both markets and individual rights.

We are moving away from justice as monopolies continue to expand and inequality rises.

We are moving away from honour as mutual respect and common principles recede from view.

We are watching duty decline as our environment penalises those who would stand by deals made and blocks those seeking to make necessary changes; increasingly, it even punishes those who would be accepting or merciful towards failure,

In the final analysis, we are reduced to the last word: Hope.

Here’s hoping.

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!