Is the Russian Ruble on the path to overvaluation ?

The appreciation movement the Russian ruble is now experiencing for several weeks stands quite firmly. The ruble broke down the 60 RR for $1 now some weeks ago. While it has advantages for Russia and may help to limit inflation, it could also have negative consequences for the Russian economy if it were to strengthen in coming months. This movement reflects both the sentiment of foreign investors (and non-resident Russian investors of course) that the Russian economy is now on a path of growth. But this movement also reflects the feeling that there would soon be opportunities for speculation in Russia.

Exchange rate developments

The appreciation of the ruble is now very clear for anyone that looks at the exchange rate in relation to the Euro or that looks at that against the Dollar. This appreciation of the Ruble seems to have been confirmed for about a year. The Ruble has just returned to its nominal exchange rate it had at the end of May 2005 in relation to the Dollar. Recovery in oil prices is to a large extent explaining that. Expressed as BRENT index, these prices rose from $32 per barrel in January 2006 to around $56 per barrel today, as a result of various OPEC and non-OPEC agreements. The rise in the exchange rate was therefore logical in this respect and could not be a surprise. Brent for April settlement dropped $0.34 to $56.24/bbl on ICE Futures Europe, which is even more significat than spot prices. The same contract advanced $0.74 to $56.58 on Thursday and is headed for a 0.8% gain this week.

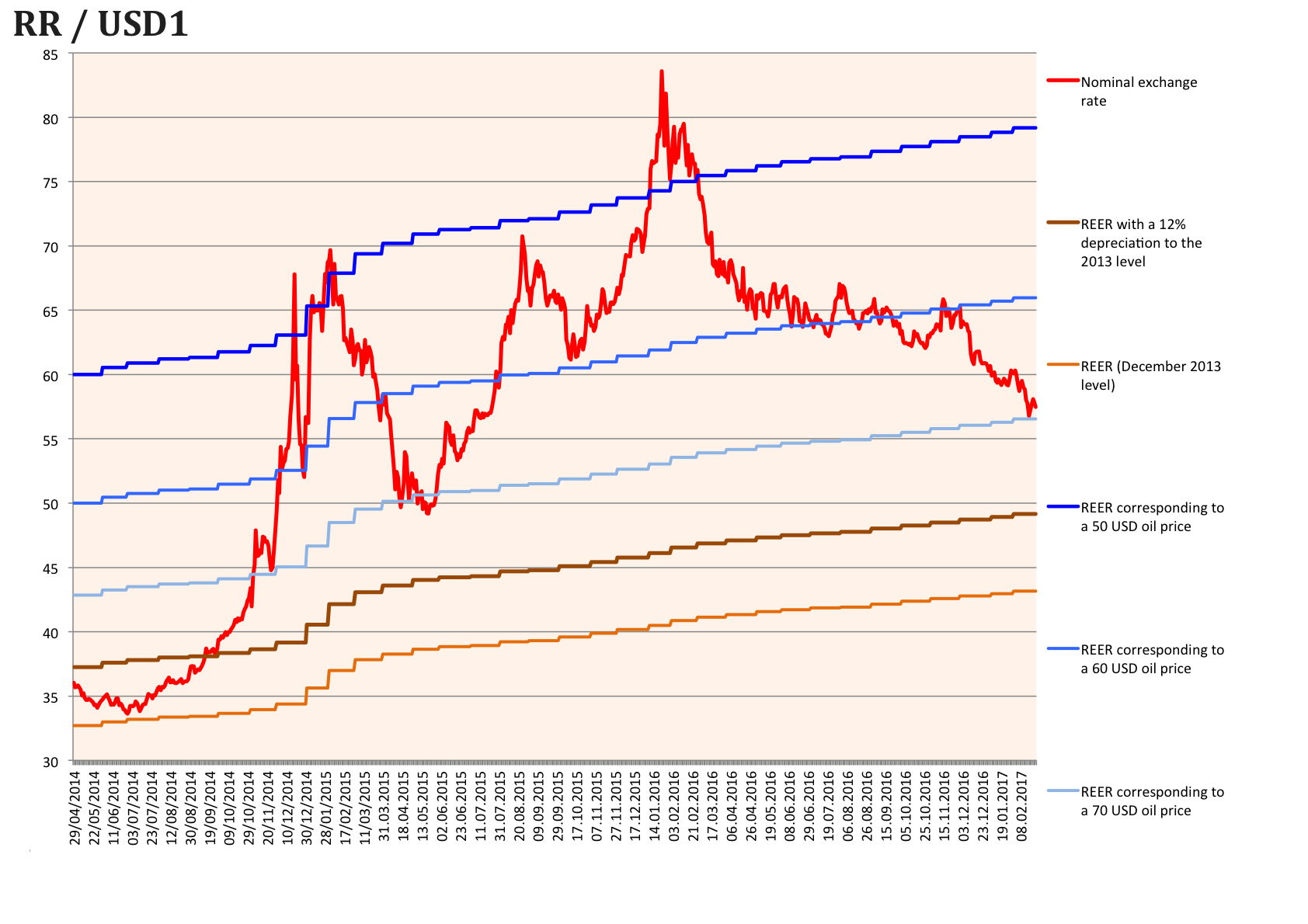

But, when comparing forecasts of the exchange rate with oil prices, we could see that the current exchange rate corresponds to a much higher oil price than what it actually is. Oil and gas extraction, while playing minor a role in economic activity, is known to play an important role in the country’s financial and budgetary balances and, above all, in managing the flow of monetary liquidity. A computational model (developed in the CEMI-EHESS) has then be used to determine the level of the exchange rate, if it were determined solely by the price of oil. Results are then displayed on the chart below.

On one hand, the nominal exchange rate is still largely undervalued compared to the real value of the ruble (that is adjusted for inflation). But, at the same time, it corresponds to what should give an oil price of 69 USD a barrel. Oil prices currently range from US $ 55 to US $ 57 per barrel (BRENT). The question therefore arises as to what explains this difference with the real price of oil, a difference of 23%.

Chart 1

Source: CEMI-EHESS

Why this appreciation of the Ruble?

There is no doubt that the weight of hydrocarbons has been reduced in the budget, and more generally its impact on the economy and the exchange rate. The predictive model used refers to mechanisms dating from 2012 to 2015. It thus tends to overestimate the impact of oil prices. The structure of the economy has itself changed since 2012-2013, and the weight of manufacturing has tended to increase not jut in the GDP but also in exports. This overestimation, probably, is now about 10%, and perhaps a little more. But this also means that there is ultimately an appreciation of the exchange rate of about 10-12% relative to its « normal » level in relation to oil prices. Thus, we can deduce there are monetary (and financial) phenomena that affect the level of the exchange rate.

- The first is certainly the fact that the Moscow stock exchange has been very largely undervalued in 2015 and 2016. Capital inflows related to share purchases are currently taking place. This phenomenon is likely to continue for at least the first half of 2017 as equity markets are under threat of major political changes in Europe (with elections in France and the Netherlands) and these same markets are largely overvalued in the United States.

- The second phenomenon is linked to interest rates. It’s very clear that the base rate of the Central Bank of Russia is today one of the highest among the emerging countries. If the real interest rate is taken into account (nominal rate minus the inflation rate), it is currently the highest for all emerging countries.

- The third phenomenon, which can be linked to the first, is the improvement of enterprise profitability in Russia, a profitability that encourages investors to take an interest in them. Investments in these enterprises will increase not only because of the low value of the shares but also because of the expected rise in dividends. Moreover, any improvement in the ruble tends to accentuate this phenomenon.

In fact, if the Governor of the Central Bank of Russia, Mrs. Elvira Nabiulina, expressed her willingness to keep the exchange rate around 60 rubles for every dollar, she does not seem to have any room to maneuver on this point.

The Dilemma of the Central Bank

Indeed, the revised figures provided by the Ministry of the Economy and the Ministry of Finance are indicating that the depression was less intense in 2016 than what has been feared. In 2015, the GDP declined by only -2.8% against -3.7% as initially indicated. As for the 2016 results, they show a stabilization of GDP (with a variation of + 0.2%) against an initial estimate of -0.6%. The approximately 0.8-0.9% difference between the first estimates and the final figures is probably due to the impact of the substitution of local products for imported products, an impact that appears to have been more important than expected and which may have surprised economists and statistician alike.

This result is both good news and bad news for the Russian economy. This is undeniably good news because it shows that the depression was much less strong than what one might have thought. But, on the other hand, this is bad news because these results will encourage the Central Bank to maintain its policy of high interest rates while observers expected a the Bank to have a more dovish behavior in 2017.

The problem is that today these high interest rates are helping to attract capital to Russia. These capital inflows are causing the appreciation of the Ruble above the “normal” level that could be deduced from oil prices. In turn, this appreciation erodes the competitiveness of the economy and could trigger a major reversal in economic dynamics. Of course, the problem is not an immediate one. The real exchange rate of the Ruble is still largely undervalued compared to its level at the end of 2013. But now we have to look at the exchange rate of 55 rubles for 1 dollar as the real alert point.

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!