Steen’s Chronicle: The Primitive economy – Outlook for next four quarters

It’s time for the final update in 2015 on the forward looking model for 2016 and to present the Primitive Economy. The very economic model we are now reduced to follow after years of poor policy response from central banks and the lack of reform from politicians:

The Primitive Global Economy, where all future scenarios is driven by one factor and one factor only: The direction of the US$.

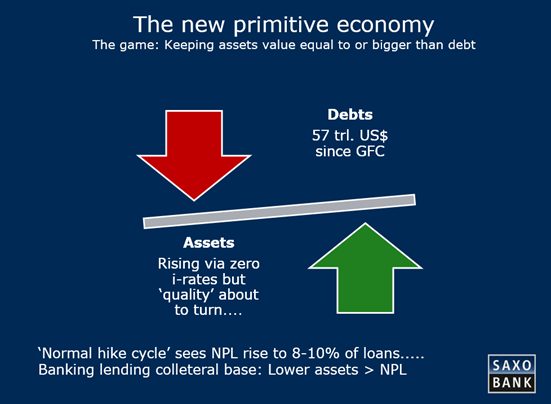

Since the Great Financial Crisis, GFC, the total global Debt/GDP has increased by 17%, that’s a cool 57.000 billion US$ of new debt – most of which has been originated in US$ and mainly raised by emerging market countries including China.

The selloff in emerging markets was really a huge margin call on US$ debt – as EM currencies collapsed 20%,30%,40% and even in some cases 50% the debt burden rose despite ‘lower yields for longer’ being the operative policy response.

Faced with an uphill struggle to repay debt emerging market reduced their investment and capex, in the process reducing the export orders for global export names in Europe and the US. The stronger US$ not only made the debt harder to repay but through inverse correlation to commodity prices it also reduced the price of oil, metals and agriculture turning the “excess savings” from China, Saudi Arabia, Norway, Mexico and Brazil into deficits.

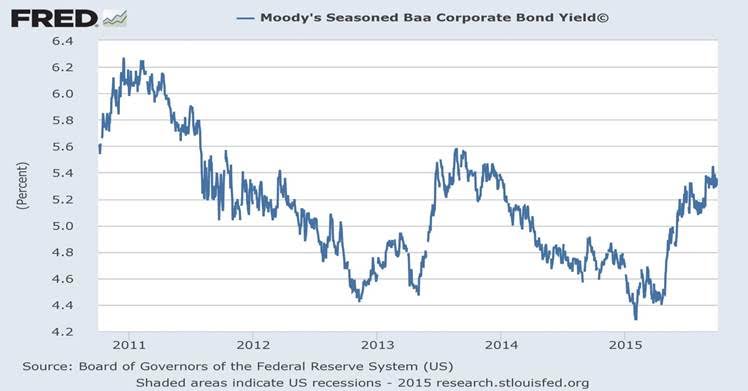

The net impact off lower global reserves being recycled has meant the cost-of-capital, COC, has risen 100 bps for lowest investment grade and 700 bps for junk rated entities.

Note how the low in spread was all the way back in June/July 2014

The correlation between lower reserves and higher yield is seen here through an excellent chart from Zerohedge:

Note: Please observe right hand scale is upside down – higher is lower yield.

This tail-wind for lower yield has in academic papers been put at an average of 100 bps discount over the cycle. I.e.: Yields, COC, has been 100 bps lower than without the recycling. This process will continue to drive the marginal cost of capital, MCC, up with or without Fed hiking rates in December.

Maybe it’s time to look at the primitive model used by policy makers:

The “game” is as follow: In an environment of ever higher debt forcing down growth, policy makers (read: central banks) lowers COC to “float” asset values. The low yield makes the forward looking value of asset go up and Voila! The world is “re-balanced” again. The problem of course being that the model is based entirely on collateral and the value of collateral is built on its present price but also its quality.

I just showed you how the junk bonds spread has risen to 1400 bps from 700 bps in less than two years – does that make the “quality” better or worse? Worse, of course, and this before Fed has even confirmed their ‘lift-off’ in rates.

What we have here is an extremely primitive economy: No one can tolerate a stronger US$ as it reduces future growth, excess savings, commodity prices and productivity……..and it happens at a time where there are major paradigm shifts about to happen:

- Fed feels forced to hike – December is now 60% likely as the starting date for lift-off – reversing seven years of easier monetary policy.

- Global ‘dis-savings’ is offsetting the stimulus by ECB and BOJ

- The asset quality is under attack as disinflation/deflation, a strong US$, and commodity prices remains near multi decade lows(high for US$). Both the earnings power needed to pay the debt but also the price of carrying the debt is working against the collateral value of the “asset” – Elementary, Dr. Watson!

This is the monetary trends, but probably underreported is the fact that Fed, and certainly BOJ is starting to think differently about the concept of “lower for longer…”

Let’s do a rewind on how and why we ended up with this misfiring forward guidance by FED, BOE, BOJ and ECB the ‘go to’ recipe when reaching zero bound interest rates.

The whole strategy of Ben Bernanke and his FED was based on a 2003 paper by Gauti Eggertson(IMF) and Michael Woodford(Princeton University) called: ‘The zero bound on interest rates and optimal monetary policy’ – the conclusion from the paper is included below:

The concept “lower for longer….” was born!

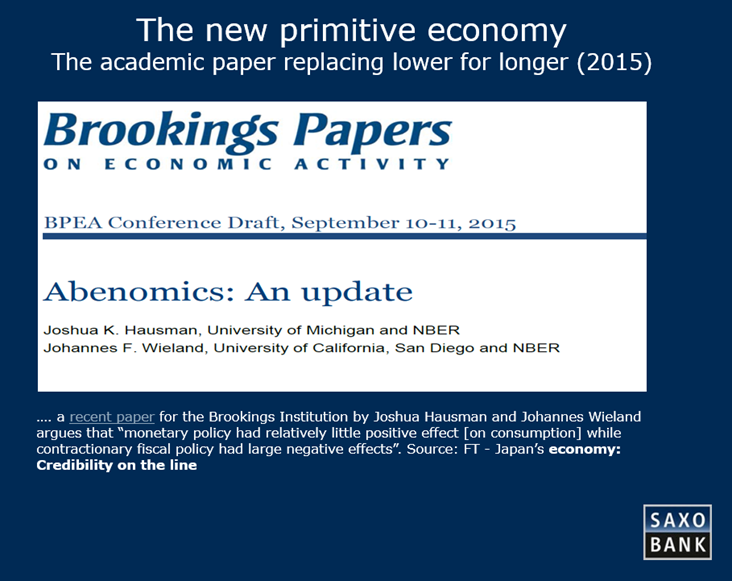

Now however, the new “mana” on the mountain is a new paper published this autumn by the Brookings Institutes Joshua Hausman, Univ. of Michicigan & NBER and Johaness Wieland, University of California & NBER titled: Abenomics: An update.

The conclusion is not surprising to people from the main street but it seems to have changed at least for now BOJ’s appetite for more stimulus!

Policy makers is always looking for an academic “anchoring” off their policy – This paper cement the position which both Draghi, Bernanke, and now Yellen continues to ad lib: Monetary policy can’t work on its own without support from fiscal policy!

Now how does this change the policy response? Clearly the US is not going to get big fiscal push one year ahead of next Presidential election and recently in Japan the market has been surprised to see Bank of Japan talking about corporates tax cuts instead of reacting to lower than expected inflation and GDP by doing more money printing.

The central banks are simply doubting the effect of low yield on the economy and is beginning to acknowledge, academically, but still ignoring publically, the unintended consequences of an economy where the allocation of capital is deficient in its root (not allocating to the principle of marginal cost of capital – and almost exclusively through an “planned” economy process) and extremely inflationary on the assets.

This is a dangerous position: The value of the asset is now not only deteriorating due to less quality (smaller earnings power, deflation/disinflation, strong US$, and price of capital) but also through an inflationary jump in valuation based on “lower for longer…” necessitated to balance out the debt (as per chart above)

The 2003 paper simply was an entry only – a one way street. There is not an orderly exit unless …… you get a weaker US$, higher productivity, a technology breakthrough or an economic model allocating money according to my good old Bermuda Triangle of economics (Stop supporting the 20% of the economy (listed companies and state owned companies) and instead focus on the 80% of the economy (The SME’s which create 85% of old new jobs and 95% of all productivity))

A highly unlike event in a political world of non-accountability and ignorance of everything economic.

Off all the listed things which can unwind/mitigate the inflated collateralized asset bubble the lower US$ not only seems the “path of least resistance” but also both the most likely and the cheapest.

How can a cheaper US$ coincide with a Fed starting to hike interest rates?

Well, the fact is the US$ is inverse correlated to the direction of US interest. In four out of the last five Fed hike cycles the peak of the US$ value has happened around the first hike – actually I seem to remember reading a paper arguing that the peak of US$ statistically comes on average 33 days before the first hike!

Yes, the primitive economy have reduced us to have one answer only to all questions regarding the future of financial markets: The US$……or more precisely the future direction of the US$.

As we leave 2015 I see these major changes to the macro environment as a conclusion to the above:

- Be long US$ into the first Fed hike – the first Fed hike is your CATALYST!

- Be short the US$ post the initial hike. Mainly vs. AUD and commodity based emerging market currencies (go short EM market currencies and markets who has benefitted the most from lower energy)

- Monitor closely the spread between lowest investment grade and junk bonds. The spread should continue to widen as asset quality weakens will increase supply (and downgrades from investment grades) creating a shortage of investable paper. Corporate debt implosion is a fat tail event which needs to be monitored!

- Expect attempts to restart fiscal expansion by governments and probably most likely in the “infrastructure space” – I expect to see big increase in public/private projects where private money funds public investments through guarantees issued by governments. Please see this excellent read on why, how and how much is needed from FT’s John Auther: Infrastructure: Bridging the gap

- Be tactical long government fixed income post the first hike from FED as it will kill the weak growth in the US setting up a flirt with negative QoQ GDP from Q4 into Q1/Q2 – but respect that this is the final move down in yield before the combined compounded forces of the above will force rates up.

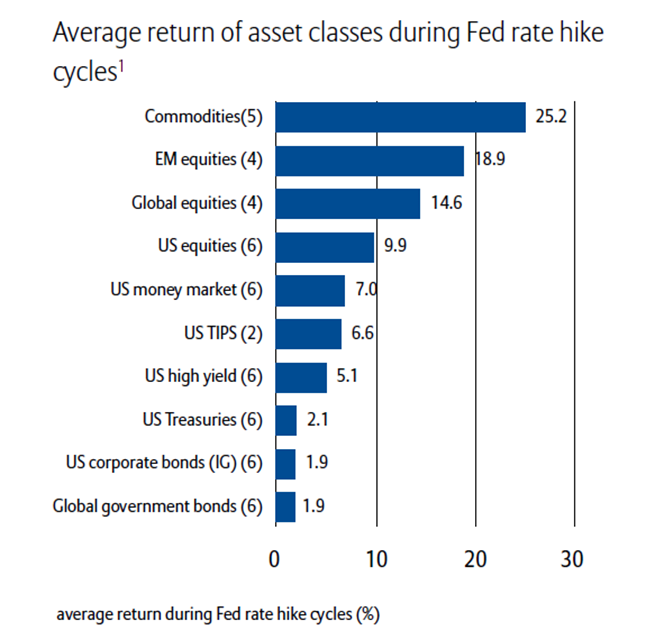

A trader could be long government bonds, but an investor will stay out as the cycle low is in place. The low will in history be June/July 2014 and the confirmation will be the first Fed hike. The commodity cycled peaked in 2011 – we now nearing the point of both price and value being attractive – use this to average into commodities and EM currencies over next six month.

Source: Historical lessons from Federal Reserve rate-hike cycles, Allianz Capital

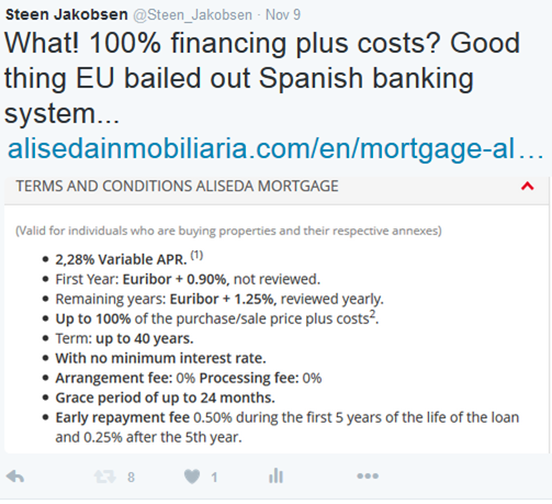

We are also a full cycle from the collapse in real estate prices in 2007/2008 but to my horror I have recently found out this week while in Madrid, that the Spanish banks now again offers mortgages at 113% of price! Yes, it’s a good thing EU/ECB bailed out the Spanish banks!

We never learn from history and Yes, reducing the burden of debt is only remedy for getting back to “normal”…..

Strategy for Q4-2015 into low in Q1/Q2-2016

By Q1/Q2-2016 we will have seen the low in:

Inflation and yield, Emerging market, Gold, silver, platinum, Growth, Energy, CAPEX, Investment

And the high in:

US$, Asset quality,Non-performing loans, Bank earnings, Dividend and buy-backs

Over time market tends to move along the path of least resistance but recently the economic gravity, the business cycle, was suspended for a full cycle through “lower for longer…”

Finally, it seems the full price of the misguided policy have compounded into a very primitive economic model. One where no one benefits from a stronger US$. Hence the path of least resistance becomes a weaker US$.

Fortunately, the weaker US$ in the cards, not only through its historic tendency to peak simultaneously with the start of a rate hike cycle but also through all the process explained above, the biggest take away from this in the next decade will be that China and the US will have to share the global leadership – The US through having the biggest and deepest capital markets, and China through its excess savings and growth. RMB will be top five currency traded by 2020 and the lesson from the expensive experience of the margin call on emerging market debt will be driving force for more local funding and deeper capital markets throughout the emerging market. Little was learned in 1997/98.

Yes, I call for the end of US$ dominance but not for the end of the US. No one ever made money from selling the US short, but their currency is now a token of a failed model and reducing the indirect help the US has gained from being global reserve currency is about to help improve the US incentive structure to reform and start a proper infrastructure and productivity drive. Cheap money did not do the job.

The world has changed dramatically on the micro level, but trust it’s for the good of things.

2015 will in history be the end of an era of too much macro and too little micro – maybe there is still time for me to get that Noble Prize in economics for my Bermuda Triangle of economics theory?

Nah, unlikely – don’t forget the Noble Prize in economics is instituted by the Swedish Riksbank and I don’t expect any favour from the Swedes, especially as we are about to face off to quality for the European Championship in football.

Safe travels,

Steen Jakobsen

Laisser un commentaire

Participez-vous à la discussion?N'hésitez pas à contribuer!